This project is a part of Duke’s Common Cents Lab. The Common Cents Lab is funded by the MetLife Foundation and supported by Blackrock as part of BlackRock’s Emergency Savings Initiative. This was first published in the 2020 Common Cents annual report. The project was done in collaboration with the Irrational Labs team, led by Richard Mathera and Lindsay Juarez.

Background

Among financial educators and within personal finance circles, budgeting – both tracking expenses and planning how much to spend in a specific category of expenses – is heralded as a way to reduce expenses and focus spending on areas of personal importance.

However, much remains unclear about the best ways to structure budgets –as well as how to help people adhere to them. Furthermore, the extent to which budgeting actually helps people to reduce expenses in the short-term – let alone in the longer term – is equally uncertain, especially given the behavioral challenges associated with creating and adhering to a budget.

We sought to explore how people approach and use budgets to guide their financial behavior. So we developed an experiment to investigate whether traditional budgeting is effective at changing behavior. We also looked at how we might use findings from behavioral research to improve budgets. As with all Common Cents Lab projects, the partner provided an anonymized data set for this project.

Hypothesis & Key Insights

We researched budgeting first through in-person interviews and auditing financial education courses. We wanted to learn how people think about budgets – and how efforts to encourage budgeting suggest that people begin using them. We also conducted online surveys and analyzed engagement and behavior through a popular fintech app.

This background work highlighted several behavioral challenges that people face when budgeting:

- Just sitting down and thinking through a budget requires significant self-control and time. Starting a budget is a daunting activity, and procrastinating is easy. Indeed, busy people already find it difficult to carve out time for things they actually want to do. They delay planning – only to realize their lack of progress six months later. Once a person has finally undertaken the seemingly monumental task of creating a budget, their struggle for self-control has only just begun. Then they have to actually adhere to it.

- Creating and adhering to a budget – requires combatting information aversion. Budgeting forces a person to take stock of previous financial decisions and reflect on life decisions that might be unpleasant to revisit. Moreover, when someone fails to follow their budget? Chances are high that they do not want to be reminded – or worse, feel ashamed – that they didn’t spend their money as planned.

- Creating a budget also requires fighting inattention and forgetting. Once a budget is actually created, a person must remember how much spending is allowed in a particular category over the budget period. They must also track – and be able to recall – how much has been spent so far across all categories for a month (or more) at a time.

Our Experiment

We worked with a popular fintech app to develop and test three different approaches to budgeting.

We randomized 9,035 people into one of three conditions:

- Informational Control (N = 4368)

- One-Number Budgeting (N = 2723)

- Category Budgeting (N = 1944)

We initiated the experiment September 30, 2019 and ran it for 13 weeks.

To eliminate selection bias, we showed Android users the same tile screen, prompting them to ‘Take control of your budget.’

Users that clicked this tile were opted into the budgeting experiment and randomized into one of the three budgeting conditions outlined below.

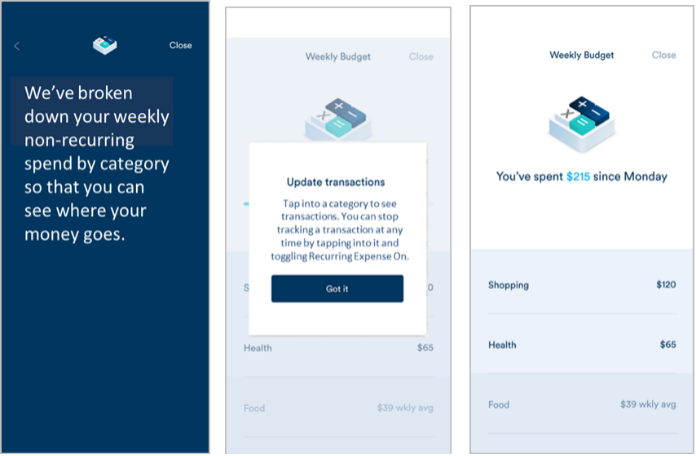

Condition 1 / Control

This was an informational control where people were presented with a sum of their overall weekly spending, broken down into transactions by category.

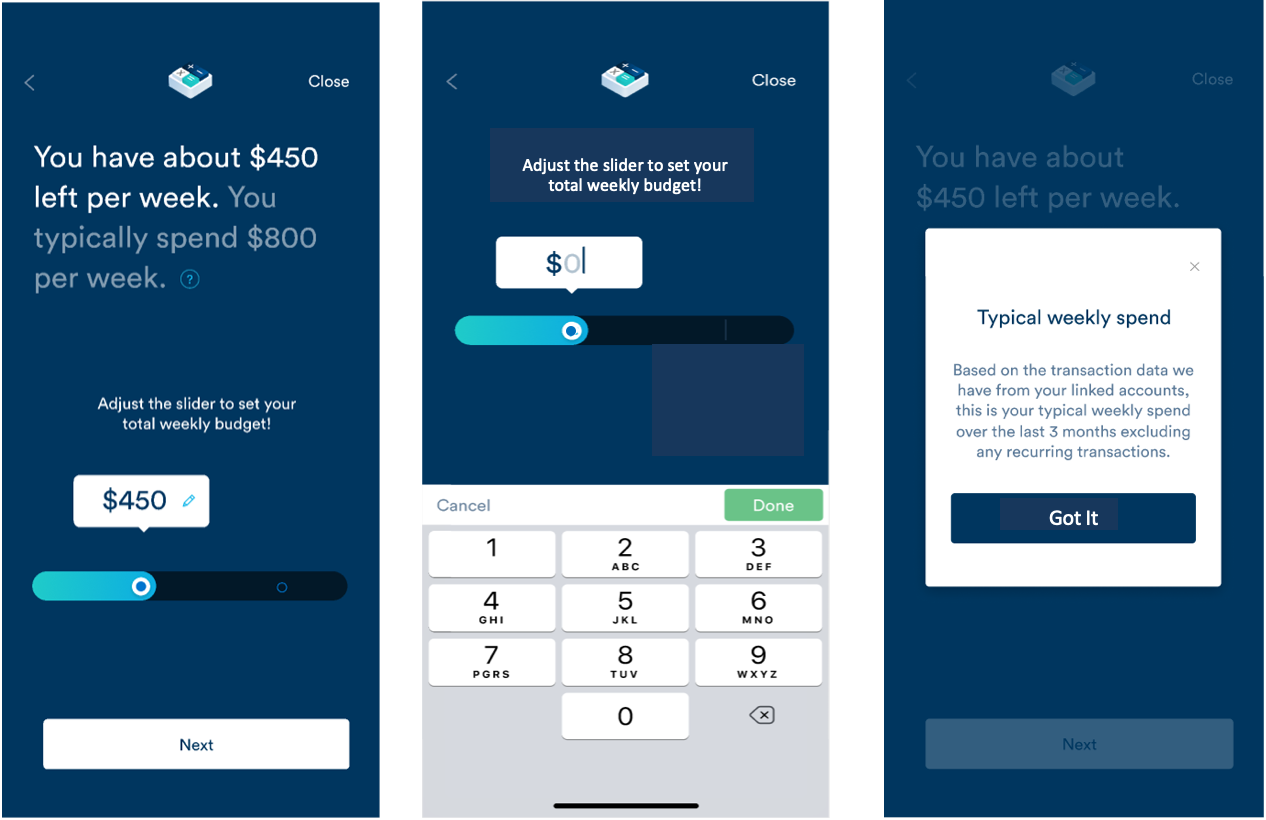

Condition 2

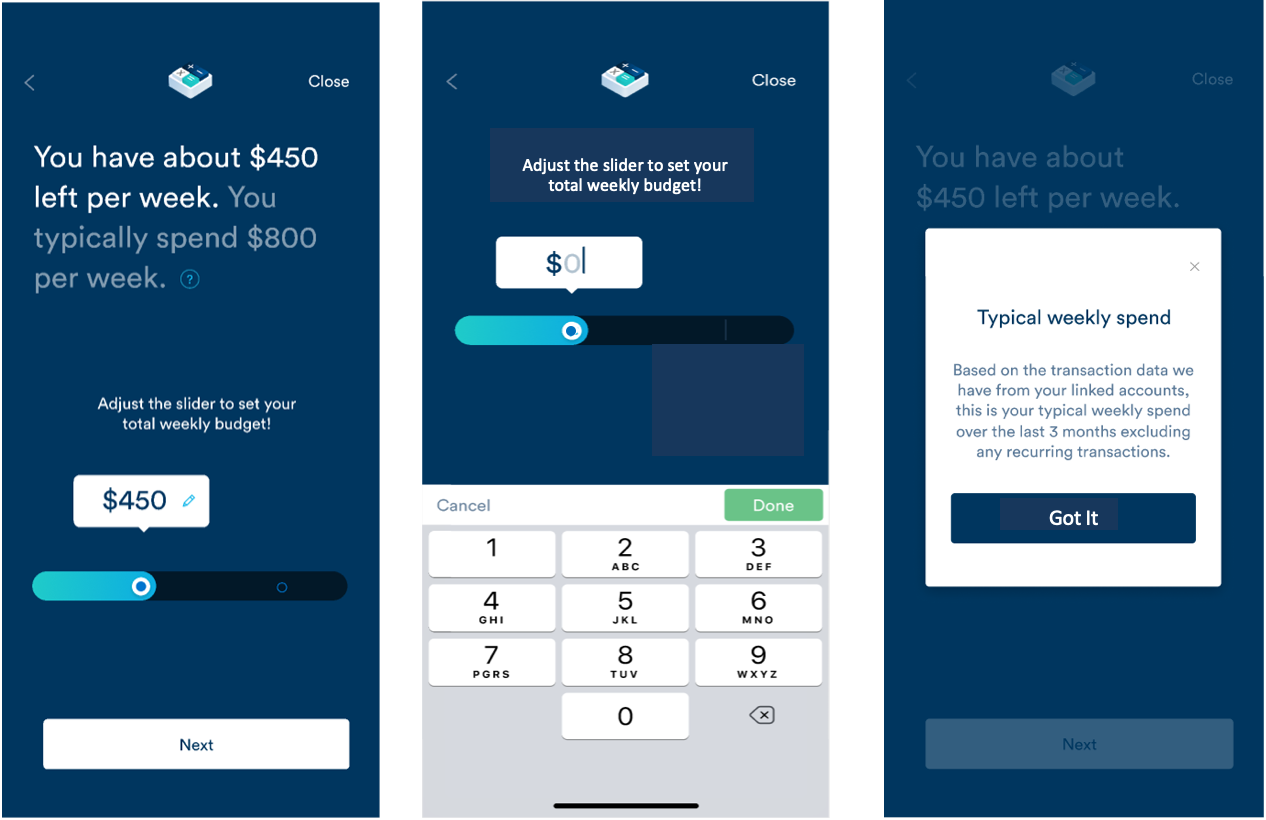

This was an ‘overall budget-setting’ condition where people were guided to set up a one-number budget for the week.

Setting the Budget

Money Feature Details View

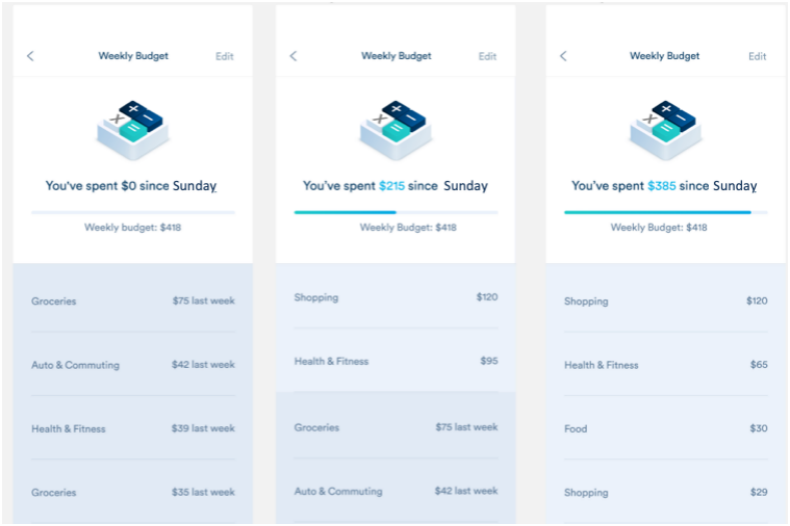

Condition 3

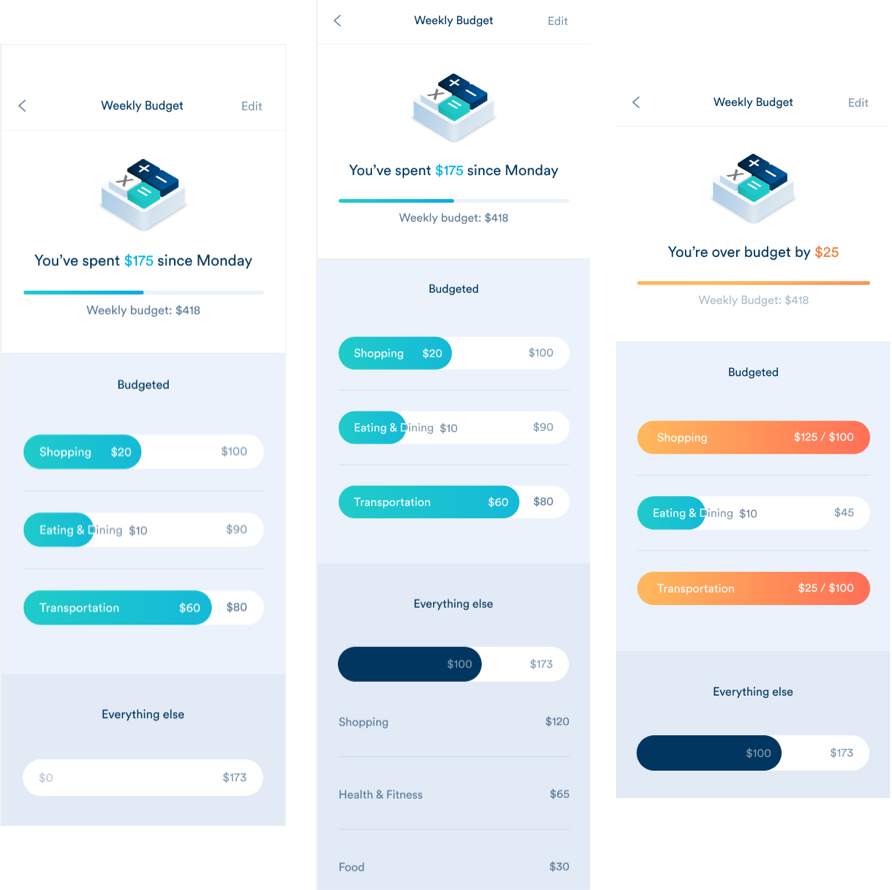

This was a ‘category-by-category’ budget-setting condition which prompted people to to set up an overall weekly budget number. Then they had to select specific categories of expenses to set goals for.

Setting the Budget

Money Feature Details View

We tracked how budgeting affected subsequent spending behavior to see whether it helped participants reduce their expenses more than an informational control.

The Results

Although some differential drop-off occurred due to effort between conditions, budgeting inherently requires some level of effort and active participation. For example, in a hypothetical two-condition paper-and-pencil budgeting intervention that placed people in two separate rooms — one in which people are asked to complete a budget, and one in which they would be asked to wait or perform some other activity such as reflection — someone who did not lift a pencil to participate in the budgeting experiment would not be considered to have budgeted.

The budgeting experiment we conducted randomized someone’s chances of being placed in one of the three conditions due to the identical opt-in screen. This feature lowered the amount of effort required to participate in budgeting as much as reasonably possible with pre-populated budgeting options. There were no observable pre-existing differences between the budgeting groups regarding income or spending patterns.

Engagement with the Budget

In terms of engagement with the budget, about 10% of the users in the experimental condition saw the budget 8 times or more, while a majority of the users (84%) saw the budget 5 times or fewer over the experimental period. Both budgeting variants statistically significantly increased engagement over the control from once every 4 weeks to once every 3 weeks (p < 0.001). In all conditions, engagement declined over time.

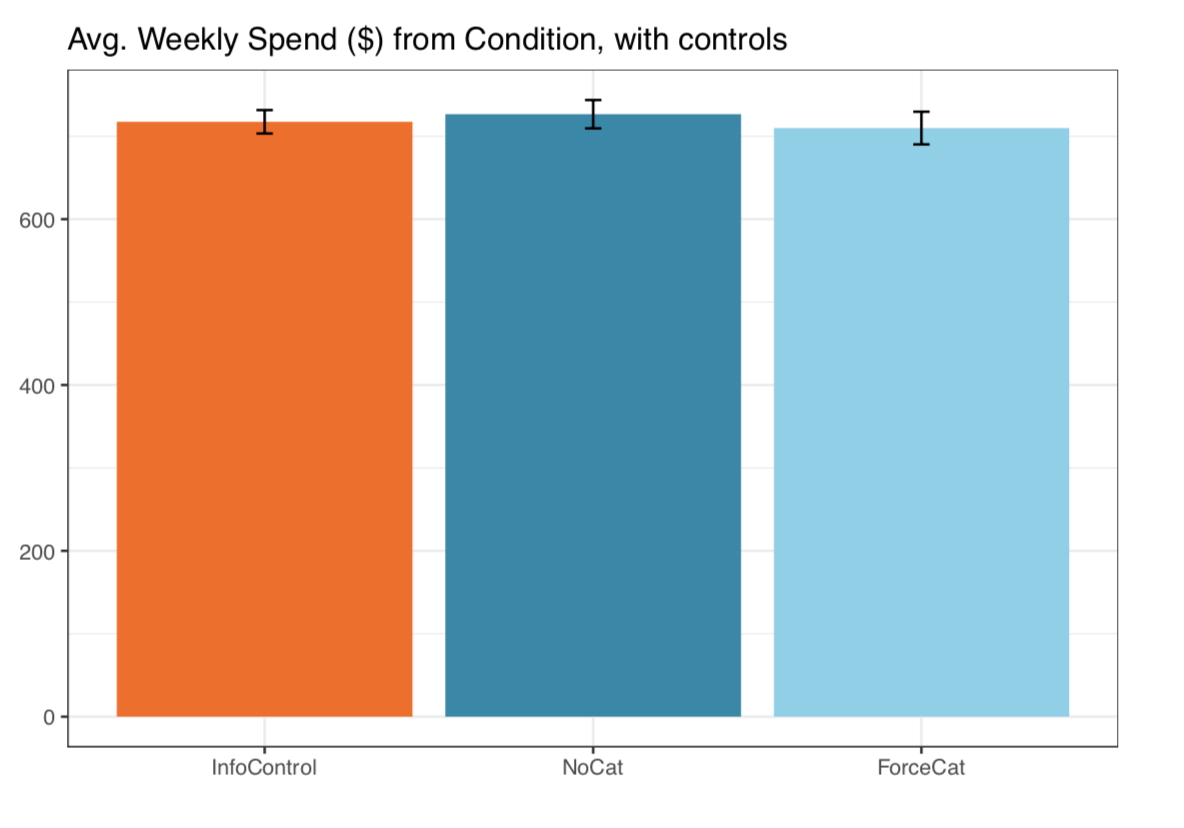

Main Finding

Overall, we found no significant difference between the average spending of the control group ($675.97) versus the single budget condition ($681.08) or the category condition ($673.25), (ps >0.4).

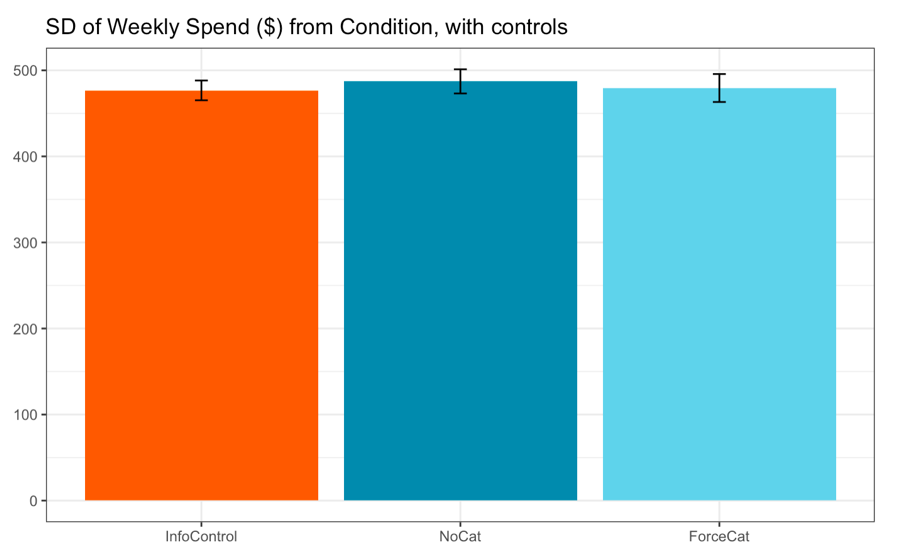

We also found no statistically significant difference in spending variability across conditions.

More Insights

The experiment led to several additional insights into budgeting behaviors:

- Budgeters generally overspent the amount they budgeted, spending 1.3-1.4 times what they intended.

- We did not see evidence that budgeters reduced their spending relative to their historic spend (ps > .15).

- We did not see spending differences by condition when we examined only the most frequently budgeted spending categories (food, groceries, shopping, and transportation) (ps > .5).

- Even after controlling for usual spending patterns, we found that spending in a budgeted category was about $30 higher than spending in non-budgeted categories (p < .001). We found no differential impact for users that checked their budgets more frequently (ps > .1).

So while the budgeting feature increased engagement with the app, overall we did not find positive or negative financial impacts from budgeting.

The good news? Proven alternatives to budgeting exist that can help us manage our money more effectively.

Want to learn more about behavioral science – and it can improve financial outcomes for products and consumers? Sign up for our finance-focused behavioral design bootcamp today.